Quantinuum’s Quantum Monte Carlo Integration Engine Shows Early Stage Quantum Advantage

Insider Brief

- Quantinuum published full details of their complete Quantum Monte Carlo Integration (QMCI) engine.

- The results suggest an early-stage quantum advantage in areas, such as derivative pricing, portfolio risk calculations and regulatory reporting.

- Monte Carlo, which problems are computationally expensive for classical machines, are often cited as a top quantum use case.

PRESS RELEASE — Quantinuum, the world’s leading integrated quantum computing company has published full details of their complete Quantum Monte Carlo Integration (QMCI) engine. QMCI applies to problems that have no analytic solution, such as pricing financial derivatives or simulating the results of high-energy particle physics experiments and promises computational advances across business, energy, supply chain logistics and other sectors.

The QMCI tool, utilizing advanced quantum algorithms, will allow quantum computers to perform estimations more efficiently and accurately than equivalent classical tools, inferring an early-stage quantum advantage in areas such as derivative pricing, portfolio risk calculations and regulatory reporting. A white paper supporting the new tool reveals that QMCI benefits from a computational complexity advantage over classical MCI, and suggests the engine has the potential to provide quantum usefulness in its current form.

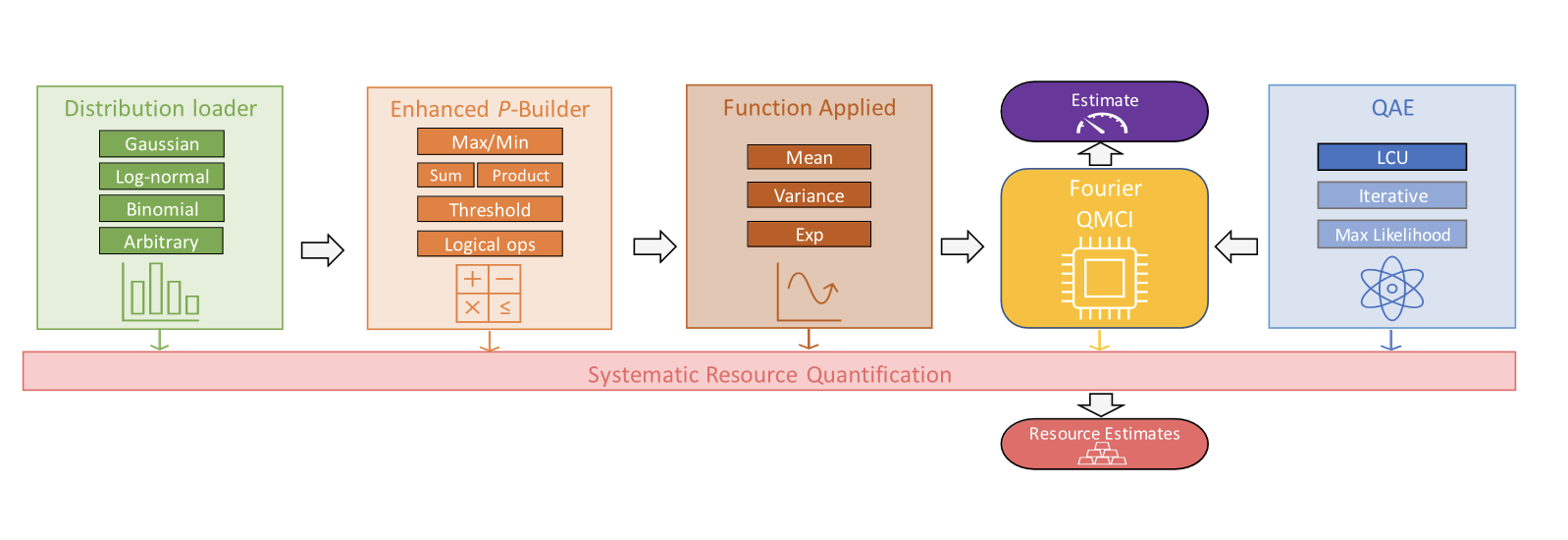

The white paper, A Modular Engine for Quantum Monte Carlo Integration, has been made available on arXiv, detailing, among other items, “the enhanced P-builder”, a tool for constructing quantum circuits representing commonplace computational methods used in finance. The white paper also proposes how users of the new tool could obtain quantum advantage without compromising statistical robustness in the ensuing estimates.

Ilyas Khan, Chief Product Officer of Quantinuum said “Quantinuum’s end-to-end QMCI engine – the first ever complete quantum solution, offers the prospect of an immediate boost to the productivity of users in at least two sectors: banking and financial institutions, and scientists who expect quantum computers to help them process the vast amounts of data generated in experimental fields such as high energy physics. Our QMCI engine is the culmination of years of work by our algorithms team, and highlights just how quantum computers will offer practical utility. Our modular approach also ‘future-proofs’ the engine as quantum computing hardware advances.”

The engine has four modules – loading probability distributions and random processes as quantum circuits; programing a wide variety of financial calculations; programming different statistical quantities (e.g. mean, variance and others); and the estimation of quantum amplitude, which is the core source of computational advantage in QMCI. The engine features a resource mode, which precisely quantifies the exact quantum and classical resources needed for user-specified calculations – a feature which is essential for predicting when particular applications will enjoy quantum advantage. Thus, the paper reveals a direct line of sight to quantum advantage and concludes users will achieve useful benefits sooner still.

Dr Steven Herbert said: “The QMCI engine taps into rapidly growing demand for tools that help global organizations in finance and other sectors explore and evaluate their route towards quantum advantage. Classical Monte Carlo integration is the preferred method in a range of computational areas where analytic solutions are unavailable and it is widely recognized that these methods will benefit from a quantum advantage. By taking a modular approach, we will equip those scientific and financial professionals with a platform that supports them flexibly through rapid technological advances in the years to come.”

Banks and financial institutions are expected to increase investment in quantum computing capabilities from $80 million in 2022 to $19 billion in 2032, growing at a 10-year CAGR of 72%.